From 1 July 2023, the general transfer balance cap was indexed meaning many more retirees can again make non-concessional contributions this year.

Contributing to superannuation is now much more accessible for older retirees with available cash and investments that they want to transfer into the tax effective superannuation environment.

Remember: The general Transfer Balance Cap (TBC) determines the amount that an individual can transfer from their superannuation savings into the ‘pension phase’ and correlates to the individual’s eligible Non-Concessional Contribution (NCC) caps based on their Total Superannuation Balance (TSB) at the previous 30 June. Put simply, you cannot make any further NCCs once your individual TSB is over the general TBC. Read Part 1 of this article here.

The opportunities

- A new opportunity arises for individuals that triggered the 3 year bring forward previously but didn’t use the remainder of their unused bring forward cap (due to their TSB at 30 June being more than the previous TBC of $1.7 million). With the TBC increasing in 2023/24, they can now make their ‘top up’ NCCs if their TSB at 30 June 2023 was less than $1.9 million.

- In addition, for those individuals who were previously ineligible for NCCs due to having a TSB of over $1.7 million, but have a balance under $1.9 million, they are again eligible to make NCCs to superannuation this year. This is quite useful for those that have personal funds they want to add to the concessionally taxed superannuation environment. This includes individuals where they had started a pension and have been drawing funds from superannuation to a point where their TSB now falls under the new TBC.

- There lies an opportunity with NCCs to be able to ‘bring forward’ NCCs to make an even larger contribution in one particular year, say because of a large asset sale if an individual wants to try to boost their superannuation as much as possible. Because of compound earnings, in most cases it is best to get the most into superannuation as soon as possible and let compound earnings do the rest, to achieve an optimal balance.

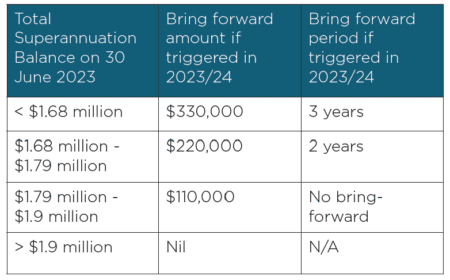

The ability to ‘bring forward’ non-concessional contributions (NCCs)

The ‘bring-forward’ NCC cap that can be triggered is determined by an individual’s TSB at 30 June.

To be eligible to ‘bring-forward’ two years’ worth of NCCs (up to $330,000 in one year) an individual’s TSB must be less than $1.68 million, as measured on 30 June of the previous financial year. If an individual’s TSB is above $1.68 million but less than $1.79 million, they can only ‘bring forward’ one year worth of NCCs (up to $220,000 in one year) as shown in the table below:

- Note that the total amount an individual can contribute in a previously triggered bring forward period will not increase because of the indexation as an individual’s ‘bring forward’ NCC limit is based on two or three times the annual cap in the year it is triggered.

- In addition, in each year of a bring forward period, the individual’s TSB must be below the TBC at 30 June of the last financial year to be able to use the remainder of their unused bring forward cap.

Superannuation contribution rules are complex. It is a good idea to seek advice. If you are interested in learning more about the types of contributions you can make, please contact us.

Prue Cheeseman is a financial adviser of HLB Mann Judd Wealth Management (NSW) Pty Ltd (AFSL 526052) ABN 65 106 772 696

This article contains general advice which does not consider your particular circumstances. You should seek advice from HLB Mann Judd Wealth Management (NSW) who can consider if the strategies and products are right for you.