The ATO have updated their guidance on PCG 2021/4 Allocation of professional firm profits – ATO compliance approach, which applies from 1 July 2022 and replaces the material published in 2015.

The PCG is the final version of a draft issued earlier this year, and unfortunately it appears that despite feedback from the major professional accounting bodies and other interested parties the ATO has not significantly softened its approach.

The new framework is used to determine an individual’s risk factor regarding profit allocation (low, moderate, or high) which influences the level of engagement individual professional practitioners (IPPs) can expect from the ATO regarding their payment arrangement.

While the outcome in each specific case will vary, it is generally expected that some practitioners who were previously regarded as low risk under the old tests may have their risk rating increased under the new guidelines.

Who does this apply to?

IPPs who breach either of the two gateways below are expected to engage with the ATO and consider their risk factor:

Gateway 1 – commercial rationale

Your current arrangement has a genuine commercial rationale and reflects the commercial needs of the business. There must be evidence that the stated commercial purpose achieves a result, usually being improvements for the business, as an outcome of the arrangement.

Gateway 2 – high-risk features

Your arrangement contains any high-risk features which are outlined in a Taxpayer Alert.

What IPPs need to know

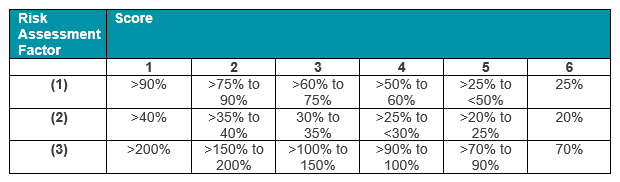

If Gateways 1 and 2 are satisfied, you may self-assess your profit arrangement to determine a risk rating, which combines the scores of the first two risk assessment factors below and, if appropriate, factor three (although factor three is optional).

- Proportion of profit entitlement from the whole of firm group returned in the hands of these IPP

- Total effective tax rate for income received from the firm by the IPP and associated entities

- Remuneration returned in the hands of the IPP as a percentage of the commercial benchmark for the services provided to the firm

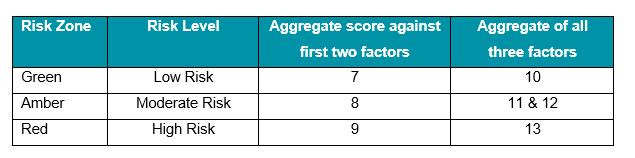

Arrangements that result in a ‘moderate’ or ‘high’ outcome is considered to be at risk of giving rise to an inappropriate tax outcome. The detailed score tables are set out below and can also be found on the ATO Website.

Risk Assessment Score for each factor

Overall Risk Assessment Score

Impact for high and moderate risk individuals

The ATO will conduct a form of compliance activity to understand the facts of your arrangement to gather understanding of the circumstances.

For more information, please visit the ATO website.

If you have any questions or concerns don’t hesitate to contact me or your HLB adviser.