Not-for-profit organisations often struggle to find the right employees because budgetary constraints restrict their ability to offer competitive salaries.

A possible solution is to utilise fringe benefits tax (FBT) exemptions, specific to the sector, which unlock extra financial resources and increase the attractiveness of the salary package to the prospective employee. However, it can be a tricky area because of the confusion surrounding what can and can’t be done. With the end of the FBT financial year fast approaching, it is a good idea to review the do’s and don’ts of FBT.

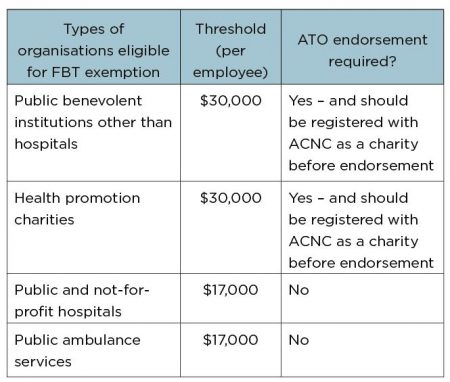

Capping thresholds

As a starting point, organisations need to assess which category of not for profit organisation they fall under. This then determines the capping thresholds applied to each employee in order to avoid incurring FBT, as shown in the accompanying table.

In addition, there is a separate single grossed up cap of $5,000 for salary packaged meal entertainment and entertainment facility leasing expenses. If this cap is exceeded, then the excess can be offset against the general cap thresholds. The next step for organisations is to ensure that whatever they offer to employees complies with any awards or enterprise agreements, and the benefits provided are effective in attracting the appropriate staff. Common examples of types of expenses offered by not-for profit organisations include mortgage repayments, provision of motor vehicles, meal cards, rent and school fees.

Other expenses

The expenses listed above would be factored into the capping thresholds as they are mostly private or non-deductible in nature. However, other expenses do not affect the capping thresholds and can sometimes be overlooked. These include purchases that employees could otherwise claim in their tax return such as membership association fees, laptop computers which only have minor private use, and professional development.

Common misconceptions

Common FBT misconceptions include:

- the cap is for non-grossed up amounts – i.e. employees believe they can salary sacrifice the total amount of the cap rather than the grossed up amount.

- when the cap is exceeded, only the excess is reported on the FBT return.

- when the meal entertainment and entertainment facility leasing cap is exceeded, it is taxed.