For anyone following local sustainability developments with a keen interest, it has been a big week.

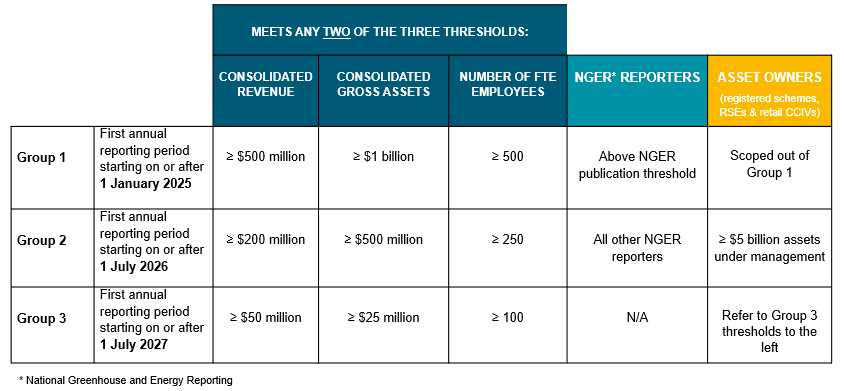

The Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Bill 2024 (the Bill) is now law, having received royal assent on 17 September 2024. Under this new law, large entities that prepare financial reports under Chapter 2M of the Corporations Act 2001 will be subject to a mandatory climate disclosure regime, with disclosure for the largest group of entities (group 1) commencing on 1 January 2025.

On 20 September 2024, the Australian Accounting Standards Board (AASB) convened and approved its two inaugural sustainability disclosure standards, namely AASB S1 General Requirements for Disclosure of Sustainability-related Financial Information and AASB S2 Climate-related Disclosures.

Although AASB S1 is similar to its international equivalent, IFRS S1, in terms of scope and content, it has been made as a voluntary standard. That is, it has not been issued by the AASB for purposes of the Corporations Act 2001 and entities caught by the new climate reporting framework will not have to comply with AASB S1 when preparing their sustainability reports under local requirements.

AASB S2, on the other hand, has been issued as a mandatory standard. Reporting entities will therefore need to apply this standard’s climate-related disclosure requirements when preparing their sustainability reports under the Corporations Act 2001.

Both AASB S1 and AASB S2 are effective for annual reporting periods beginning on or after 1 January 2025, with earlier application allowed.

In terms of assurance requirements, the Auditing and Assurance Standards Board (AUASB) has issued an exposure draft detailing its proposed roadmap for audits and reviews of sustainability reports prepared by entities for financial years commencing from 1 January 2025 to 30 June 2030.

Under the AUASB’s proposals, the scope and extent of assurance prior to 1 July 2030 will be phased in as follows:

- Limited assurance over scope 1 and scope 2 emissions from the first year of reporting, progressing to reasonable assurance in the second year of reporting;

- Limited assurance over governance and strategy (risks and opportunities) from the first year of reporting, progressing to reasonable assurance in the fourth year of reporting; and

- Limited assurance over all other disclosures from the second year of reporting, progressing to reasonable assurance in the fourth year of reporting.

This phased approach will allow time for uplift in skills and capabilities, maturity of systems and processes and refinement of sustainability-related data quality.

These recent developments all point to one thing: the time to start preparing is now.

For many entities, it will be their first interaction with ESG, meaning significant capability building and upskilling will be needed. Given the evolving definition of risk and its wider financial implications, boards and executives should be leading the charge when it comes to building in-house knowledge and engaging staff.

Developing a reporting roadmap is a helpful starting point to get things moving. This involves understanding your mandatory reporting requirements and when they commence, and then mapping out what steps you need to take to ensure you are ready to begin reporting.

Rather than approaching climate reporting as a compliance exercise, entities should set themselves up for future success by starting to integrate ESG considerations into their business strategies and risk management processes. This will require whole-of-organisation involvement, bringing the financial and strategy functions together. Taking this proactive approach will enable entities to lay the groundwork for future sustainability reporting requirements beyond climate change.

While group 2 and group 3 entities have some time before mandatory climate reporting kicks in, the effort required to get reporting-ready should not be underestimated. We encourage entities to start their climate reporting journeys now to ensure they can confidently meet the new disclosure requirements and effectively communicate their sustainability story.